For Filipinos searching for quick pautang online or emergency cash, Finbro has become one of the rising names in the digital lending market. Known for its fast approval, minimal requirements, and SEC registration, Finbro promises to provide easy access to loans without the hassle of bank paperwork.

- What Is Finbro?

- How to Apply for a Finbro Loan

- Finbro Loan Requirements

- Finbro Loan Interest Rates & Fees

- Disadvantages of Finbro

- Finbro vs Other Loan Apps

- User Reviews of Finbro

- Tips to Maximize Approval in Finbro

- FAQ About Finbro Loan App

- Is Finbro legit?

- What is the maximum loan amount?

- How fast is the approval process?

- Does Finbro require proof of income?

- What happens if I miss my payment?

- Can I repay via GCash or 7-Eleven?

- Conclusion

In this review, we’ll take a deep look at Finbro’s loan features, requirements, interest rates, advantages, disadvantages, and how it compares to other loan apps in the Philippines.

What Is Finbro?

Finbro is an online lending platform in the Philippines operated by Sofia Finance Inc., a lending company registered under the Securities and Exchange Commission (SEC).

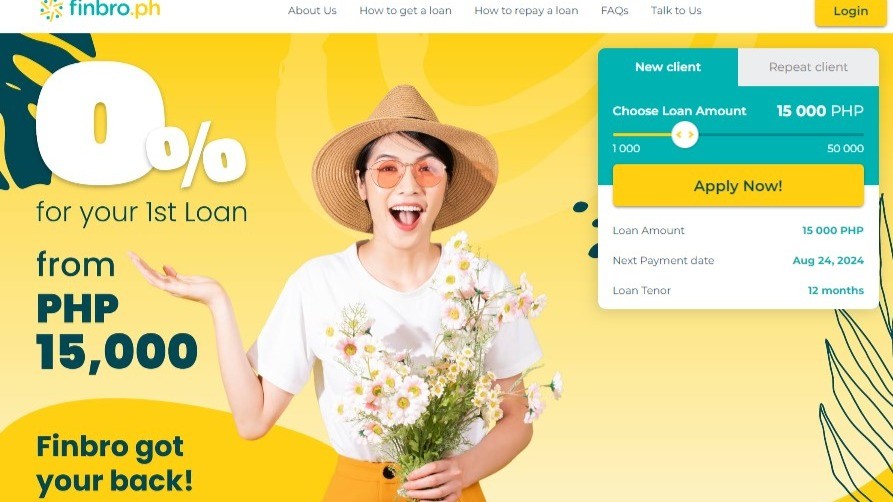

- Loan amounts: ₱1,000 – ₱50,000

- Repayment terms: 30 days to 12 months

- Interest rates: 0.5% – 1.25% per day (depending on profile and loan term)

- Special offer: 0% interest on the first loan for new borrowers

- Disbursement: Bank transfer, GCash, or e-wallets

How to Apply for a Finbro Loan

The application process is fully online and takes less than 15 minutes.

Steps:

- Go to the Finbro website or download the app.

- Register using your mobile number and valid email.

- Provide basic personal and employment information.

- Upload a valid government-issued ID.

- Get instant credit evaluation.

- If approved, loan is disbursed within 24 hours (sometimes instantly for repeat borrowers).

Finbro Loan Requirements

- Filipino citizen, age 20–65

- Valid government ID (UMID, Driver’s License, Passport, etc.)

- Active mobile phone number and email address

- Stable income source (employed, self-employed, freelancer, OFW support)

Finbro Loan Interest Rates & Fees

| Loan Amount | Term | Interest Rate | Processing Fee | Total Repayment |

| ₱3,000 | 30 days | 1.25%/day | ₱100 | ₱3,975 |

| ₱10,000 | 90 days | 0.8%/day | ₱200 | ₱12,600 |

| ₱20,000 | 6 months | 0.6%/day | ₱300 | ₱25,500 |

| ₱50,000 | 12 months | 0.5%/day | ₱500 | ₱68,750 |

⚡ Note: First-time borrowers can avail of a 0% interest loan, usually capped at ₱3,000.

Advantages of Finbro

- SEC-registered and legitimate

- High maximum loan (up to ₱50,000) compared to other apps

- Flexible repayment terms up to 12 months

- 0% interest promo for first-time borrowers

- Fast approval and disbursement

Disadvantages of Finbro

- High daily interest (up to 1.25%) compared to banks

- Processing fees reduce the actual disbursed amount

- First loan limit is usually small (₱1,000–₱3,000)

- Customer service feedback is mixed

Finbro vs Other Loan Apps

| Feature | Finbro | Tala | Digido | Cashalo | JuanHand |

| Max Loan | ₱50,000 | ₱25,000 | ₱25,000 | ₱15,000 | ₱15,000 |

| Repayment Term | 30 days – 12 months | 21–30 days | 7–180 days | 15–45 days | 91–120 days |

| Interest | 0.5%–1.25% daily | 11%–15% monthly | 0% first loan; up to 1.5% daily | 3.95%–5.42% monthly | 9%–12% monthly |

User Reviews of Finbro

- ⭐ “I got approved instantly and received ₱3,000 in my GCash. Very helpful for emergencies.”

- ⭐ “Interest is high if you extend the loan. Make sure to repay on time.”

- ⭐ “Their 0% first loan is a good deal, but customer support was hard to reach.”

- ⭐ “I like that they offer up to ₱50,000. Good option if you need bigger loans compared to Tala or Cashalo.”

Tips to Maximize Approval in Finbro

- Upload a clear government ID.

- Provide accurate employment and income details.

- Repay your first loan early to unlock higher limits.

- Keep your contact information consistent.

- Borrow only what you can repay to avoid penalties.

FAQ About Finbro Loan App

Is Finbro legit?

Yes, Finbro is operated by Sofia Finance Inc., registered with the SEC.

What is the maximum loan amount?

₱50,000 for eligible repeat borrowers.

How fast is the approval process?

Usually within 24 hours, often instantly for loyal borrowers.

Does Finbro require proof of income?

Not always, but providing proof increases approval chances.

What happens if I miss my payment?

Late fees and high interest apply, and collection reminders are frequent.

Can I repay via GCash or 7-Eleven?

Yes, repayment is available via e-wallets, banks, and partner centers.

Conclusion

Finbro is a legitimate and flexible online loan app in the Philippines that offers higher loan amounts and longer repayment terms than most competitors. With its SEC license and 0% promo for first-time borrowers, it’s a strong option for those who need bigger loan ceilings. However, borrowers should be cautious of the high daily interest rates and always repay on time to avoid penalties.

👉 Compare the best loan apps in the Philippines →