Being self-employed in the Philippines comes with freedom and flexibility — but also financial challenges. Freelancers, small business owners, and entrepreneurs often face irregular income and stricter requirements when applying for a loan. Many banks and lending apps still prefer traditional employees with fixed salaries.

- What is a Personal Loan for the Self-Employed?

- Benefits of Personal Loans for Self-Employed Filipinos

- Challenges for Self-Employed Loan Applicants

- Best Banks and Lenders for Self-Employed Borrowers

- Requirements for Self-Employed Personal Loan Applications

- How to Apply for a Personal Loan as Self-Employed

- Tips to Increase Approval Chances

- Risks and Considerations

- Alternatives to Personal Loans for Self-Employed

- FAQ on Self-Employed Personal Loans

- Can self-employed people really get personal loans in the Philippines?

- What documents do I need as a freelancer?

- What is the minimum income requirement?

- How much can I borrow?

- How long is the repayment period?

- Are interest rates higher for self-employed?

- Which is better — bank loan or online lending app?

- Conclusion

However, personal loans for self-employed individuals are possible if you know where to apply, what documents to prepare, and how to improve your chances of approval. This guide will walk you through the best lenders, interest rates, requirements, and practical tips to secure funding for your business or personal needs.

What is a Personal Loan for the Self-Employed?

A personal loan is a type of pautang online or bank loan that does not require collateral. For self-employed borrowers, it provides access to cash for:

- Expanding a small business

- Paying suppliers or contractors

- Covering personal emergencies

- Debt consolidation (utang management)

- Home or lifestyle improvements

Unlike salary loans, where income is verified through payslips, self-employed applicants must prove business stability and income consistency through other documents like bank statements or tax returns.

Benefits of Personal Loans for Self-Employed Filipinos

Why Self-Employed Borrowers Choose This Option

- No collateral needed – Unsecured loans are available for qualified borrowers.

- Flexible use – Can be used for personal or business purposes.

- Build credit history – Timely repayment helps improve credibility with banks.

- Higher loan amounts – Some banks offer up to ₱2 million.

- Structured repayment – Predictable monthly amortizations compared to informal lending.

Challenges for Self-Employed Loan Applicants

While there are clear benefits, self-employed individuals face unique hurdles:

- Unstable income – Lenders prefer steady salaries.

- More documents required – Banks need proof of business operations.

- Lower approval rates – Especially for startups or freelancers without long history.

- Higher interest rates – Some lenders see self-employed borrowers as higher risk.

This is why choosing the right lender and preparing strong documents is crucial.

Best Banks and Lenders for Self-Employed Borrowers

| Lender / Bank | Interest Rate (monthly) | Loan Amount | Terms | Requirements (Self-Employed) |

| BDO Personal Loan | ~0.59% – 1.3% | ₱10,000 – ₱1M | 6–36 months | DTI/SEC registration, ITR |

| BPI Personal Loan | ~1.2% | ₱20,000 – ₱1M | Up to 36 months | Bank statements, business docs |

| Security Bank | ~1.3% | ₱30,000 – ₱2M | 12–36 months | ITR, audited FS, COE (if applicable) |

| EastWest Bank | ~1.5% | ₱25,000 – ₱2M | 12–36 months | Business permits, bank records |

| Tonik Bank (Digital) | ~1.7% | ₱5,000 – ₱250,000 | 6–24 months | Bank transfers, e-wallet statements |

| Home Credit / Fintech Apps | ~2% – 5% | ₱5,000 – ₱150,000 | 6–24 months | Valid ID, proof of transactions |

(Note: Rates vary by applicant profile and lender policies.)

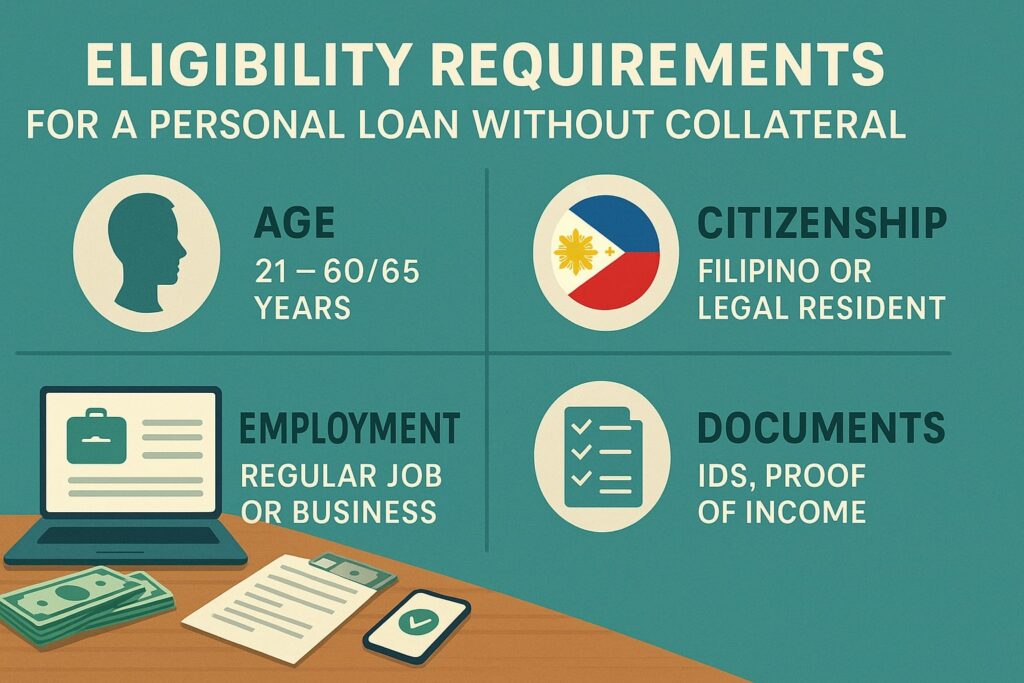

Requirements for Self-Employed Personal Loan Applications

Unlike salaried employees, the self-employed must provide more documentation to prove financial stability.

Common Requirements

- At least 21 years old (not older than 65 upon loan maturity)

- Filipino citizen with residence in the Philippines

- Minimum income: ₱25,000–₱30,000 monthly (varies by bank)

- Valid IDs (UMID, Driver’s License, Passport, PRC)

- DTI or SEC registration for businesses

- Mayor’s Permit or other business permits

- Income Tax Return (ITR) or audited financial statements

- Bank statements (3–6 months)

- Proof of billing

Some digital banks and fintech apps may accept alternative proofs of income, like GCash or Grab transaction history.

How to Apply for a Personal Loan as Self-Employed

Step-by-Step Guide

- Check eligibility – Age, income, and business status.

- Gather documents – Focus on showing income consistency.

- Compare lenders – Look for the lowest interest rates and flexible terms.

- Apply online or in-branch – Banks allow both options.

- Wait for approval – Ranges from 3 to 7 banking days.

- Receive funds – Credited directly to your bank account.

Pro tip: Applying with your main business bank increases approval chances.

Tips to Increase Approval Chances

- Maintain clean bank transactions (avoid bounced checks).

- Pay taxes and keep ITR updated.

- Avoid multiple simultaneous applications.

- Borrow only what you can repay.

- Keep good credit standing (pay bills and cards on time).

Risks and Considerations

- High penalties for late payments – Always pay on time.

- Debt cycle – Don’t borrow more than necessary.

- Variable income pressure – Plan amortizations based on lean months.

Alternatives to Personal Loans for Self-Employed

- Pag-IBIG Multi-Purpose Loan – for Pag-IBIG members.

- SSS Flexi-Fund / Loans – if you are an SSS member.

- Credit cards – good for short-term borrowing if paid fully each month.

- Online lending apps – fast but higher rates.

- Pawnshop loans – quick cash but risky due to collateral.

FAQ on Self-Employed Personal Loans

Can self-employed people really get personal loans in the Philippines?

Yes. Many banks and digital lenders offer loans to freelancers, entrepreneurs, and small business owners — as long as you provide proof of income and business stability.

What documents do I need as a freelancer?

You will need valid ID, bank statements, and in some cases, tax filings or business permits. Digital lenders may accept GCash or PayPal records.

What is the minimum income requirement?

Most banks require ₱25,000–₱30,000 monthly income. Digital lenders may accept lower income proof.

How much can I borrow?

Loan amounts range from ₱10,000 to ₱2 million, depending on your documents and credit history.

How long is the repayment period?

Typically 6 months to 36 months, but some banks allow up to 5 years.

Are interest rates higher for self-employed?

Yes, usually slightly higher than for salaried employees, since lenders see freelancers as higher risk.

Which is better — bank loan or online lending app?

Banks offer lower interest rates, but approval is harder. Apps are faster but more expensive.

Conclusion

For self-employed Filipinos, getting a personal loan may seem challenging, but it’s absolutely possible with the right preparation. By choosing the right lender, preparing strong documents, and maintaining good financial discipline, you can secure affordable financing to grow your business or cover personal needs.

Ready to take the next step? Compare the best loan apps in the Philippines →