Many Filipinos search for fast cash solutions during emergencies, tuition deadlines, or unexpected expenses. One of the most popular financial products is the personal loan without collateral, also known as an unsecured loan (pautang online or utang).

- What is a Personal Loan Without Collateral?

- Benefits of a Collateral-Free Personal Loan

- Risks & Things to Consider

- Eligibility Requirements for a Personal Loan Without Collateral

- Best Personal Loan Providers Without Collateral in the Philippines

- Personal Loan Without Collateral vs Secured Loan

- Tips to Get Approved for a Collateral-Free Personal Loan

- Application Process – Step by Step

- FAQ – Personal Loan Without Collateral

- 1. Can I get a loan without collateral if I have bad credit?

- 2. What is the minimum salary requirement for unsecured loans?

- 3. Is it safe to apply for online personal loans?

- 4. What happens if I fail to repay?

- 5. Do self-employed individuals qualify?

- 6. How much can I borrow without collateral?

- 7. Which bank is best for a personal loan without collateral?

- Conclusion

This type of loan allows you to borrow money without pledging any property, car, or savings as security. It’s convenient, flexible, and widely available in the Philippines through banks, government agencies, and online lending apps.

In this article, we’ll explain everything you need to know about personal loans without collateral: their benefits, requirements, top lenders, and how to increase your chances of approval.

What is a Personal Loan Without Collateral?

A personal loan without collateral is an unsecured loan where approval is based on your income, credit history, and repayment ability, not on assets like land, houses, or vehicles.

Borrowers can use the funds for almost any purpose, including:

- Paying medical bills

- Education and tuition fees

- Home renovations

- Debt consolidation

- Travel or personal needs

Tip: Since there is no collateral, lenders rely heavily on your creditworthiness and employment stability when deciding approval.

Benefits of a Collateral-Free Personal Loan

- No need for assets – Ideal for employees and renters who don’t own property.

- Quick approval – Some online loan apps approve within 24 hours.

- Flexible use – Money can be used for any purpose.

- Build credit history – On-time payments improve your credit score.

- Higher accessibility – Both employed and self-employed individuals may qualify.

Risks & Things to Consider

While unsecured loans are attractive, borrowers must be cautious:

- Higher interest rates compared to secured loans.

- Stricter income requirements from banks.

- Late payment penalties can grow quickly.

- Negative credit score if you fail to repay.

- Collection actions may be taken by lenders.

Always calculate your monthly budget before applying for a loan without collateral.

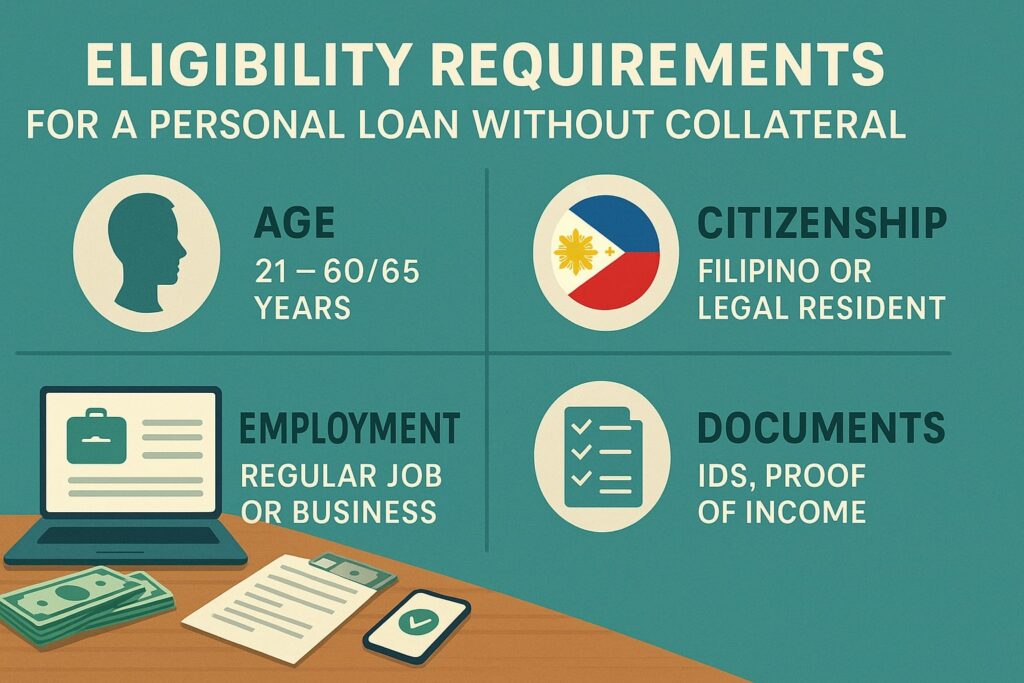

Eligibility Requirements for a Personal Loan Without Collateral

General Qualifications

- Age: 21–60 years old.

- Income: At least ₱15,000–₱20,000 monthly (varies by bank).

- Employment: Regular employee (6–12 months tenure). Self-employed applicants must provide business permits and ITR.

- Residency: Must be a Filipino citizen or permanent resident.

- Credit standing: A clean credit history increases approval chances.

Standard Document Requirements

- Valid government-issued ID (UMID, Driver’s License, Passport).

- Proof of income (latest payslips, Certificate of Employment).

- Proof of billing (utility bills).

- Bank account details for disbursement.

- For self-employed: DTI/SEC registration, ITR, bank statements.

Best Personal Loan Providers Without Collateral in the Philippines

Here’s a comparison of popular banks and lending apps offering unsecured personal loans:

| Lender | Income Requirement | Loan Amount | Interest Rate | Processing Time |

| BDO | ₱15,000/month | ₱10k – ₱1M | 1.25%–2% monthly | 5–7 days |

| BPI | ₱20,000/month | ₱20k – ₱2M | 1.2% monthly | 5–10 days |

| Security Bank | ₱15,000/month | ₱30k – ₱2M | 1.39% monthly | 5–7 days |

| UnionBank | ₱15,000/month | ₱20k – ₱1M | 1.29%–1.79% monthly | 5–7 days |

| EastWest Bank | ₱15,000/month | ₱25k – ₱2M | 1.49% monthly | 5–7 days |

| Online Loan Apps (e.g. Tala, Cashalo) | ₱8,000–₱10,000/month | ₱2k – ₱50k | 3%–20% monthly | Instant–24 hrs |

Personal Loan Without Collateral vs Secured Loan

| Feature | Unsecured Loan (No Collateral) | Secured Loan |

| Collateral Required | No | Yes (house, car, property) |

| Approval Time | 1–10 days (faster with apps) | Longer (due to asset verification) |

| Interest Rate | Higher (1.2%–3% monthly) | Lower (0.8%–1.5% monthly) |

| Loan Amount | ₱2k – ₱2M | ₱100k – ₱10M+ |

| Risk | Credit score damage if unpaid | Loss of collateral if unpaid |

If you need quick cash without risking assets, unsecured loans are the safer option.

Tips to Get Approved for a Collateral-Free Personal Loan

- Keep a good credit score.

- Borrow only what you can repay.

- Prepare complete documents.

- Apply with a bank or lender that matches your income level.

- Avoid multiple simultaneous loan applications.

Pro Tip: Some lenders offer salary-deduction schemes for employees, which increase approval chances.

Application Process – Step by Step

- Choose a lender – Compare banks, apps, or government agencies.

- Check eligibility – Ensure you meet age, income, and employment criteria.

- Prepare documents – Valid ID, payslips, proof of billing.

- Apply online or in-branch – Submit application form.

- Verification process – Employer and income will be checked.

- Approval & disbursement – Funds are sent via bank account, check, or e-wallet.

- Repayment – Monthly amortization or salary deduction.

FAQ – Personal Loan Without Collateral

1. Can I get a loan without collateral if I have bad credit?

Yes, but it’s harder. Some online lending apps may approve low amounts despite poor credit, but with higher interest rates.

2. What is the minimum salary requirement for unsecured loans?

Banks typically require ₱15k–₱20k monthly income, while online apps may accept as low as ₱8,000.

3. Is it safe to apply for online personal loans?

Yes, if you use legitimate, BSP-registered lending apps. Always check reviews before applying.

4. What happens if I fail to repay?

You may face penalties, higher interest, collection calls, and a negative credit history that affects future loans.

5. Do self-employed individuals qualify?

Yes. They must submit DTI registration, ITR, and bank statements as proof of income.

6. How much can I borrow without collateral?

- Banks: ₱20,000 – ₱2 million

- Online apps: ₱2,000 – ₱50,000

7. Which bank is best for a personal loan without collateral?

BPI, Security Bank, and UnionBank are popular choices for unsecured loans due to competitive interest rates and flexible terms.

Conclusion

A personal loan without collateral is one of the most convenient ways for Filipinos to access extra cash. It doesn’t require assets, making it ideal for employees, renters, and freelancers.

However, since it carries higher interest rates, borrowers should carefully compare banks and online lending apps before applying. Always borrow responsibly and ensure you can repay on time.

Compare the best loan apps in the Philippines →